Collaborative Approaches to Cost Management

Progressive supply management departments across multiple industries such as automotive, electronics, and pharmaceutical have learned the hard way that the most effective way to reduce costs for strategic commodities is not through price haggling, but through effective collaboration. When supply management, engineering, and suppliers put their heads together to find innovative ways to reduce costs, the outcome is generally mutually beneficial for both parties: The buying company gets a lower price, and in many cases, the supplier benefits from a higher margin and a guarantee of future business. Two of the most common approaches to collaborative cost management include target pricing and cost-savings sharing.

Target Pricing Defined

Target pricing is an innovative approach used in the initial stages of the new-product development (NPD) cycle to establish a contract price between a buyer and seller. Japanese manufacturers, in an effort to motivate engineers to select designs that could be produced at a low cost, originally developed target pricing methodologies during the 1980s to battle the rising yen versus the U.S. dollar. These innovators came up with a simple concept to apply in new-product development: The cost of a new product is no longer an outcome of the product design process; rather, it is an input to the process. The challenge is to design a product with the required functionality and quality at a cost that provides a reasonable profit. In a new car, for example, the development team may work with marketing to determine the target price of the vehicle for the product’s market segment. Using final price as a basis, the product is disaggregated into major systems, such as the engine and power train. Each major system has a target cost. At the component level (which represents a further disaggregation from the system level), the target cost is the price that a purchaser hopes to attain from a supplier (if the item is externally sourced).

With target pricing, a product’s allowable cost is strictly a function of what a market segment is willing to pay less the profit goals for the product. Under traditional pricing approaches, however, product cost + profit = selling price. Using a target pricing approach, the selling price − profit = the allowable product cost. Generally speaking, the target cost is not always achievable by the supplier in early negotiations. Moreover, the supplier’s current price to provide a product or service today is probably greater than the target price set forth by the buying company.

The difference between the supplier’s price and the target cost becomes the strategic cost-reduction objective. This gap must be reduced by both parties in a collaborative effort through such methods as value engineering, quality function deployment, design for manufacturing/assembly, and standardization. Setting product-level target costs that are too aggressive may result in unachievable target costs. Setting too low a strategic cost-reduction challenge leads to easily achieved target costs but a loss of competitive position. In setting target prices and target costs, the new-product development team should bear in mind the cardinal rule of target costing: The target cost can never be violated. Moreover, even if engineers find a way to improve the functionality of the product, they cannot make the improvement unless they can offset the additional cost.

One of the pioneers and industry leaders in target pricing is Honda of America Manufacturing (described in the opening paragraph to this chapter). The company breaks product costs down to the component level. Suppliers are asked to provide a detailed breakdown of their costs, including raw materials, labor, tooling, and required packaging as well as delivery, administrative, and other expenses. The breakdown of costs is helpful in suggesting ways that suppliers can seek to improve and thereby reduce costs. Cost tables are jointly developed with suppliers and used to find differences (line by line) across all elements of cost. A potential area of disagreement involves the supplier’s profits and overhead. A fair profit is required but may be dependent on the level of investment. No fixed profit level is used in negotiations. Supply management must then aggregate the parts costs and compare them with the target costs. If total costs exceed target costs, the design must change or costs must be reduced. Although the supplier’s profit margins might be an easy place to look for cost savings, Honda realizes that doing so would squander the trust it worked hard to develop with suppliers.

Once a purchaser has established a target price with a supplier for the first year of a contract, additional cost reductions over the life of the product can be made through an ongoing effort to drive down costs year over year. This can be achieved through a technique known as cost-savings sharing.

Cost-Savings Sharing Pricing Defined

Cost-savings sharing differs from traditional market-based pricing in several ways. First, cost-sharing approaches require joint identification of the full cost to produce an item, which is not the case with market-based pricing (where the buyer has little or no knowledge of the supplier’s costs). Second, profit is a function of the productive investment committed to the purchased item and a supplier’s asset return requirements (i.e., return on investment). Profit is not a direct function of cost (which is usually the practice with market-driven prices). The cost-based approach provides a supplier with incentives to pursue continuous performance improvement to realize shared cost savings and invest in productive assets. A later example illustrates these concepts.

An important feature of cost-savings sharing is the financial incentives offered to a seller for performance improvements above and beyond the improvements agreed to in the purchase contract. This differs from the traditional market-based pricing approach where one party (usually the purchaser) seeks to capture all cost savings resulting from a supplier’s improvement effort. Traditional pricing practices have been a deterrent to cooperative efforts to make design, product, and process improvements. A cost-savings sharing approach recognizes the need to provide financial incentives to a supplier while enhancing closer relationships.

Prerequisites for Successful Target and Cost-Based Pricing

In order for target and cost-based pricing to occur, there must be joint agreement on a supplier’s full cost to produce an item. Identification of all costs provides the basis for establishing joint improvement targets. The total cost to produce an item includes labor, materials, other direct costs, any costs due to start-up and production, and administrative, selling, and other related expenses.

Besides total cost components, the parties must jointly identify and agree upon product volumes, target product costs at various points in time, and quantifiable productivity and quality improvement projections. Each firm must also agree on the asset base and return requirement at the supplier that determines an item’s profit.

There must also be agreement on the point in time when mutual sharing of cost savings takes place, as well as the formula used to share the rewards. Mutual sharing of rewards usually occurs for savings above and beyond the performance improvement targets agreed to in the purchase contract, and savings on any items incidental to joint performance improvement targets.

This approach requires a high degree of trust, information sharing, and joint problem solving. This process will fail if one firm takes advantage of the other or violates confidentiality of information sharing. There must also be a willingness to provide the resources necessary to resolve problems affecting overall success.

The ability to manage the risks associated with target pricing is another key prerequisite. Perhaps the main risk concerns volume variability. Because volume affects cost levels, both parties must carefully consider and manage the impact of changes from planned volume projections. Higher-than-projected volumes will result in a supplier achieving greater economies and lower per-unit costs. These lower costs, however, are not the result of a supplier’s performance improvement. Conversely, lower than projected volumes may raise a supplier’s average costs. Contractually, the parties must determine how to manage changes from the buying plan.

When to Use Collaborative Cost Management Approaches A cost-based approach to determining price is clearly not appropriate for all purchased items. Many items do not warrant cost analysis, or the marketplace determines price. Based on the cost management portfolio matrix discussed earlier in the chapter, it is obvious that products that are readily available from multiple sources, standardized instead of customized, and heavily influenced by the market forces of supply and demand do not fit the profile of items appropriate for cost-based pricing. What types of items are feasible for a cost-based cooperative approach? A cost-based approach is feasible when the seller contributes high added value to an item through direct or indirect labor and specialized expertise. This approach is particularly appropriate for complex items customized to specific requirements. Also, products requiring a conversion from raw material through value-added designs at a supplier are possible candidates. Examples of such items include a specially designed antilock brake system or a dashboard for an automobile. These items require a high value-added conversion from raw materials into a semifinished product. The supplier also likely contributes design and engineering support.

An Example of Target Pricing and Cost-Savings Sharing

Although actual target and cost-savings sharing agreements can be lengthy and complex, the following example demonstrates the fundamental principles of this strategic cost management approach. This example is based on an actual situation that occurred between an automotive OEM and a first-tier supplier.

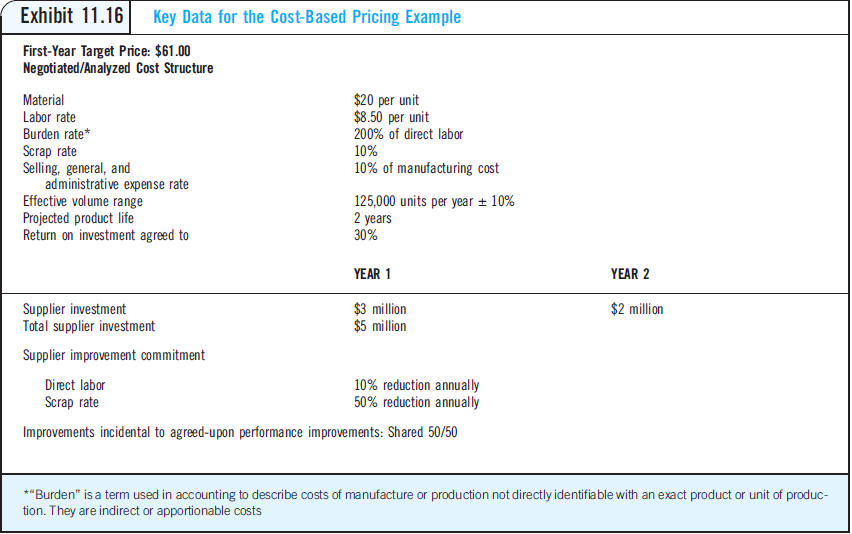

A purchaser seeks to purchase a designed component that is part of a final end product. The final selling price of the product has been determined through discussions with marketing, and this figure has been rolled down (or disaggregated) to the component level. As such, both parties have agreed to target a purchase (or selling) price of $61 for the component for the first year. The purchaser has targeted this price as one that will support meeting the overall target price of the final end product.

Cost-savings sharing assumes that the buyer and seller will collaborate to identify the most efficient processes to produce a product as the basis for the cost structure. This approach does not reward inefficient processes or practices, and also assumes that engineers at the buying organization are flexible and willing to modify product specifications to align with the supplier’s processes. Throughout this example the supplier’s costs and return requirements serve as the basis for determining a fair and competitive price. Both parties agree to a negotiated cost-based approach because the parties have developed a close working relationship, supporting the sharing of detailed cost data, and because the supplier’s cost structure is relatively efficient.

Exhibit 11.16 details the costs and investment data needed to develop a cost-based purchase contract.

Both firms must identify the costs and supplier investment associated with the purchased component, identify and agree on the supplier’s asset return requirements, and identify supplier commitments to annual performance improvement targets.

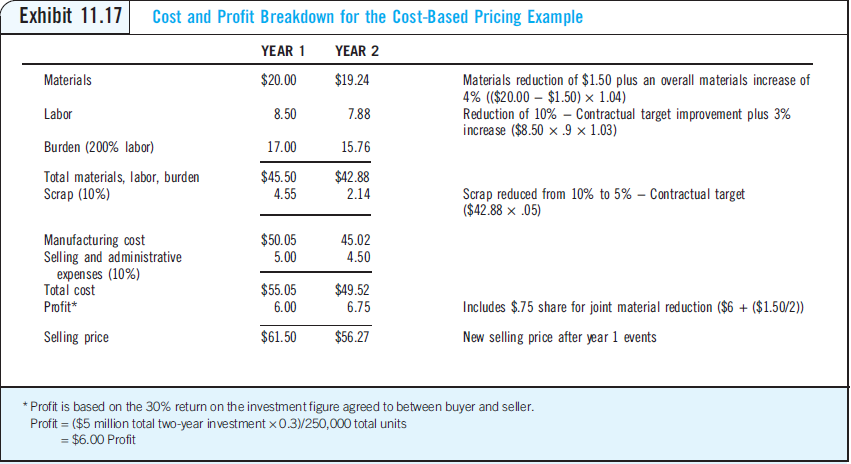

These exhibits provide the basis for evaluating cost and price throughout the life of the contract. Exhibit 11.17 details the cost breakdown and subsequent price of the component for each year of this contract. Data for year one include the negotiated/analyzed information presented in Exhibit 11.16. During the first year, the following events affected the selling price at the start of year two:

• Overall material costs rise by 4 percent due to raw material cost increases.

• A joint value analysis team identifies a substitute material that reduces material costs by $1.50 per unit.

• Labor rates increase by 3 percent per unit due to a scheduled contractual increase at the supplier.

• The supplier meets the agreed productivity improvement targets for reduced scrap and improved labor productivity.

Year Two data include these events:

• The supplier receives 50 percent of the $1.50 material reduction identified by the value analysis team.

• The profit figure for year two includes the supplier’s share of the material reduction.

• The selling price at the start of year two becomes $56.27.

By focusing on joint and continuous performance improvement, the purchase price was reduced at a time when material and labor costs actually increased. This example illustrates the potential for improvement that can occur through joint price/cost analysis.

Establishing agreement on cost and price early in design and development supports the reduction of material costs through cooperative efforts. The use of cost-savings sharing can induce both parties to work together to achieve mutual goals. The purchaser reduces its cost curve for purchased items and also establishes a basis for continuous cost-improvement initiatives. The supplier benefits from longer-term contracts, a fair profit based on its asset investment, and increased competitiveness due to improvements occurring because of the purchaser’s insights and contributions.

Good Practice Example Best Practices in Strategic Cost Management Leadership

A recent benchmarking study carried out interviews with 13 organizations in a variety of industries to identify current practices in strategic cost management. The population of companies was segmented based on whether their cost management practices were considered “Basic,” “Moderately Advanced,” “Advanced,” or “Most Advanced.” The key differences and transitional elements noted for firms in each category were documented and are highlighted in this executive summary. We focus here on the key steps required to progress from a “Basic” level of cost management, through different stages of maturity, and the core capabilities that must be developed through this evolution

MOVING FROM “BASIC” TO “MODERATELY ADVANCED”

Firms in the “Basic” category seeking to move to the next level were generally focused on “establishing the foundation,” through a focus on getting back to the basics of spend analysis, data cleansing, and establishing simple governance structures for cost management. This includes the following actions:

• Governance – Establish a Demand Management program to drive business unit leaders to create realistic budgets for spending, new product introductions, and forecasting of requirements to enforce a discipline of cost budgeting.

• Systems – Initiate a corporate-wide cost systems effort focused on data cleansing of all historical pricing, spend AP data, and labor rates to establish the backbone of a cost management support system.

• Supply Base Management – Establish a program for supply base consolidation, with specific targets defined by business, by category, and by platform.

• Leadership and Planning – Establish a corporate champion for cost leadership as a priority for competitive success across all key functional lines of business, with a governance committee to drive oversight and support.

• Metrics – Establish Key Performance Indicators for cost management alignments with financial projections, profit targets, line of business NPI projects, and market growth targets.

• Talent – Establish a network of key subject matter experts from across the organization with the requisite talent and skills, to build a cost management organization to provide decision-support to NPI, sourcing, and make or buy projects.

• NPI – Conduct a major audit of NPI processes to ensure that cost targets are tied product design outcomes, with accountability for cost established for the NPI team.

MOVING FROM “MODERATELY ADVANCED” TO “ADVANCED”

Firms in the Moderately Advanced category have established the core foundational elements required to build a cost management culture and system and should seek to establish the next level of cost capability through the following activities:

• Governance – Organizational realignment to ensure cost engineers are aligned by material or process globally, with specific roles, responsibilities, and accountability to business. Realignment to also create a joint material handling, packaging, procurement and logistics costing team tasked with building total cost models for all major point to point sourcing movements for major shipments around the globe.

• Systems – Accurate spend analytics database with updated and historical spend by category, by part family, by supplier, and by business accessible by all relevant functional teams.

• Supply Base Management – Segmented supply base with strategic approved suppliers (established quality, cost, and technology), approved suppliers, and emerging suppliers.

• Leadership and Planning – NPI planning team to establish projected key capacity bottlenecks and supplier cost overruns, based on NPI new product forecasted projections, data collected from impacted facilities, cost engineering leads, cost management team associates, and global sourcing category leads. This team should have a rolling five-year view on all upcoming new projects; highlight impacted areas, and key areas of immediate and pending concern.

• Metrics – Documented internal labor and material cost histories for all major facilities and product lines established and available through efforts of IT/team.

• Talent – Talent development efforts to establish key engineering cost manager roles in procurement, including competitor teardown and should-cost modeling, cost target objective setting, VA/VE, material and labor costing, and collaborative design.

• NPI – Initial engagement of strategic suppliers to attend NPI team meetings, with the objective of establishing consistent input and feedback for achieving cost targets.

MOVING FROM “ADVANCED” TO “MOST ADVANCED”

Firms in the Advanced category have established a cost leadership organization, processes, systems for supporting cost decisions, and key performance indicators and are poised to engage on the next level of key activities to establish cost leadership in their industry:

• Governance – Global sourcing offices staffed with multilingual expats and local sourcing professionals aligned with NPI product requirements for supplier engagement in emerging countries.

• Systems – Cost management systems that drive part commonality, re-use, preferred suppliers, cost histories, and regular updates available to all NPI, sourcing, and manufacturing/engineering teams across the globe.

• Supply Base Management – A set of long-term supplier partnerships with active involvement on all NPI teams, engaged in on-site technical and material management support for cost management in NPI and production.

• Leadership and Planning – A documented category strategy and cost improvement plan for every part currently in production or going into production.

• Metrics – Detailed cost breakdowns, pricing histories, commodity and labor forecasts on all preferred suppliers with cost containment strategies available on a rolling three-year basis.

• Talent – Clear career path and leadership plan to attract the most highly talented individuals into the cost engineering roles.

• NPI – Development of Advanced Manufacturing Engineering teams that work in the supplier and technology community to track new developments, cost trends, and emerging technologies that need to be identified and nurtured for development. Active supplier development teams working at supplier locations through major NPI product ramp-up, launch, and post-launch.

Questions

Is the transformation of an organization to cost leadership a procurement responsibility, or a shared responsibility?

What is the role of change management and cultural changes in driving cost leadership?

Discuss the key elements that are required to transform an organization which is just beginning this journey? What do you think is the critical success factor? Source: Handfield, R., and Edwards, S. (2009, July), “Cost Leadership Best Practices,” White Paper, Supply Chain Resource Cooperative, NC State University